Spikes and valleys in M&A and dealmaking activity have been fairly routine and expected occurrences over the years in the biopharmaceutical sector. Just when they’ll strike, however, and the trajectories triggered as a result, are becoming less easy to pin down these days. That’s due in large part to a wildly evolving and complex operating environment for life sciences companies in projecting and ultimately executing on their product strategies, whether market- or development-focused. The argument could be made that would-be M&A participants today are tasked with navigating and acting on the most volatile mix of business drivers and influences—internally and on macro levels—in the industry’s history.

As far as the headwinds involved, they include looming mass patent expirations for Big Pharma flagship medicines; the still-tenuous market and IPO climate for already cash-strapped biotechs, particularly early-stage, small-cap companies; and hope and caution around further interest-rate movement in the US. Hurdles are also emerging as a result of Inflation Reduction Act (IRA) legislation in the US and potential impacts from November elections; heightened M&A and dealmaking scrutiny by the Federal Trade Commission; and continued broader geopolitical and regulatory uncertainty.

All these forces swirling together, experts agree, raise the urgency of sound decision-making—on dealmaking. And not just for the fates of the parties involved, but in benefiting the greater biopharma ecosystem and efforts to sustain the industry’s innovative lifeblood and future commercial viability.

“The big thing for companies now, given these headwinds, is the business cannot wait and sit on the sidelines for too long,” says Subin Baral, global life sciences deals leader, EY, citing the impending “patent cliff” in particular, where, he says, between 2024 and 2028, the revenue at risk for the top 25 global biopharma companies will total about $300 billion. “These industry fundamental issues are not waiting for anybody.”

Subin Baral

Global life sciences deals leader

EY

Pharma companies are seemingly heeding that message, as many of the challenges mentioned haven’t deterred dealmaking pursuits. Instead, activity has notably surged in recent months, echoing the theme of EY’s latest annual Firepower report, spearheaded by Baral, of “back in business.”1 After a flurry of deals announced in mid-to-late December, Baral notes that total M&A value for 2023 reached $215 billion, up 51% from 2022 and closer to pre-COVID-19 pandemic levels. The deals included:

- AstraZeneca’s acquisition of cell therapy-focused Gracell Biotechnologies for up to $1.2 billion.

- Bristol Myers Squibb’s purchase of brain drug developer Karuna for $14 billion, along with a separate agreement to buy RayzeBio, a radiopharmaceuticals company.

- Roche acquiring certain subsidiaries of LumiraDx focused on point-of-care diagnostics for $295 million.

Though deal volume grew only 2% last year, 2023’s agreements were significantly larger, notes Baral. Cases in point: Amgen’s $27.8 billion acquisition of Horizon Therapeutics and Pfizer’s $43 billion purchase of Seagen, completed in October and December, respectively, and both after initial FTC antitrust concerns; and AbbVie’s $10 billion buyout of ImmunoGen, announced in late November.

Adding to the momentum more recently was a spate of high-profile deals unveiled at the J.P. Morgan Healthcare Conference in early January. Those included:

- Johnson & Johnson’s $2 billion acquisition of antibody-drug conjugate (ADC) specialist Ambrx.

- Merck & Co.’s purchase of cancer biotech Harpoon Therapeutics for $680 million.

- GSK’s acquisition of Aiolis and its asthma pipeline.

- A pair of deals struck by Novartis—a $250 million buyout of Calypso Biotech and a $185 million RNAi-focused licensing agreement with Shanghai Argo.

Just this week, news broke of Sanofi’s acquisition of Inhibrx, worth up to $2.2 billion, and Merck’s macrocyclic peptide partnership with Unnatural Products for $220 million.

The reported positive vibes and renewed optimism expressed by C-suite leaders on hand at the JPM event aligned with expert expectations for biopharma M&A in 2024. PwC, in its yearly Deals Outlook Report, projects activity levels in the $225 billion to $275 billion range across subsectors.2 Executives, PwC predicts, will continue to deploy cash balances and pursue areas of innovation and clinical differentiation to help address growth threats in the latter half of the decade.

In its Industry Credit Outlook 2024 report, released in January, S&P Global Ratings also sees the M&A wave sustaining power in the near term, pointing to the strategic need for companies to accumulate economies of scale, and secure higher reimbursement rates from payers, despite the elevated interest rate environment.3

Michael Abrams

Managing partner

Numerof & Associates

“Many organizations are seeing extraordinary cash inflows—and given the depressed valuations of smaller firms, it really has been a Big Pharma’s buyers’ market,” Michael Abrams, managing partner, Numerof & Associates, tells Applied Clinical Trials. “Consolidation within the industry, I think, is going to continue—with particular interest in oncology, rare disease, and immunology.”

CLOSING THE GAP(s)

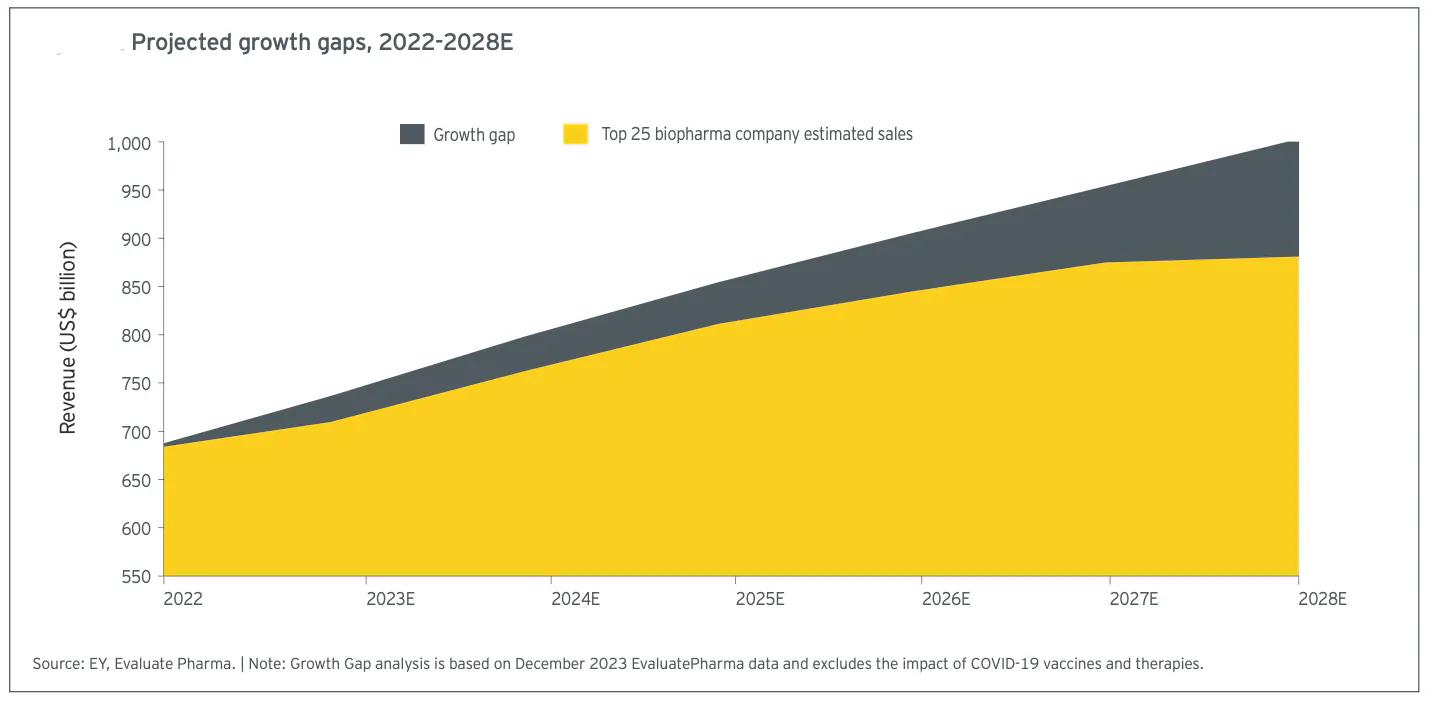

Despite healthy footing in the immediate future—for example, Baral points out that the industry, according to EY reporting, has $1.37 trillion in capital available for dealmaking—the looming patent cliff is poised to widen biopharma’s “growth gap” considerably. The growth gap is defined as the difference between forecasted company revenue streams, along with projected sales from internal therapeutic candidates currently in clinical trials, and the revenue at risk from patent losses to top-selling, established brands and subsequent competition from generics and biosimilars. EY’s Firepower report projects that Big Pharma will be faced with a growth gap of more than $120 billion by 2028, doubling from the $60 billion estimated by 2026.

“What that means is there’s not enough [quality] pipeline in the R&D system to be able to bridge the gap that that we expect the industry will have. That is a prime trigger for access to external innovation, M&A, partnership, etc.” Baral tells ACT.

At the same time, Baral is quick to remind that these organizations—the traditional pharma behemoths—“didn’t wake up yesterday thinking, ‘holy cow, now we have a risk of a patent cliff.’” In reality, they have long factored such events into their ongoing planning and problem-solving in product lifecycle management. Today, these efforts are more routinely prioritizing the need for specialization, and, hence, in M&A pursuits, a sharpened focus on areas where companies can add tangible value.

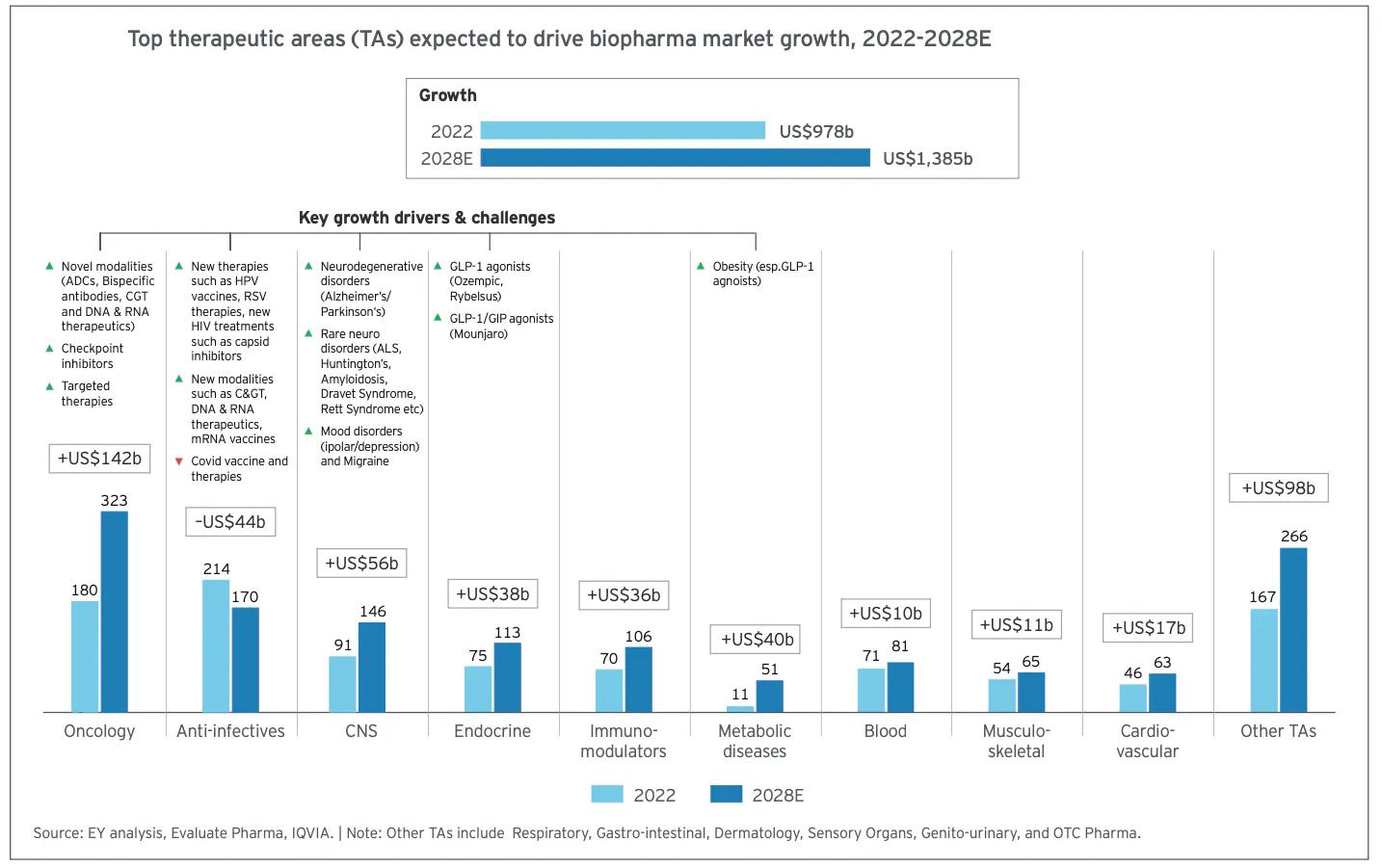

“The key, going forward, is that the assets with the right science and the right data behind them will continue to get a lot of traction and valuation,” says Baral, citing in particular the treatment promise, and, by extension, increased dealmaking interest, in therapeutic settings such as:

- New and maturing ADC platform approaches in cancer.

- Novel advances emerging for neurological and psychiatric disorders, as well as rare diseases.

- Burgeoning opportunities for collaboration (though contingent on broader strategic fit) in the GLP-1 space for weight loss and other indications beyond already established entrenchment in diabetes.

“The onus is now back on the sellers to really prove that their asset has legitimacy to take it to the next phase of development, so that they can entice the buyer pool to come to the table,” says Baral.

The path from there, if a deal is ultimately struck—and the job of beginning to secure and maximize the long-term value—remains a major theme of biopharma M&A. In many cases, the stories are still being written.

“It could be a multibillion-dollar multinational buying a startup, development-stage company with a different culture, different dynamics, and a different focus,” says Baral in describing one scenario. “How do you manage and balance the integration process so that you don’t lose the continuity of the development spirit, the passion for science that these entrepreneurial companies have—and so they don’t get stifled by the big corporate red tape, if you will, that can hinder the development cycle?”

A LENS ON LICENSING

Not surprisingly, licensing and partnership arrangements, centered on acquiring or collaborating on drug or technology assets, are also garnering increased interest in the current business climate, with particular appeal to prospective buyers. According to data from Syneos Health’s 2024 Dealmakers’ Intentions Survey, 2023 experienced a significant uptick in deal value generated from partnerships.4 Such agreements, collectively, totaled close to $400 billion last year, up more than 60% from 2022. Syneos surveyed 169 members of the biopharma community who participate on one or both sides of a deal. Among emerging areas of partnering Syneos identifies is cell and gene therapies, with 67% of respondents stating they are actively or opportunistically seeking deals in the space. Interest likely grew further after UK and US regulators approved the first-ever CRISPR/Cas9 gene-editing treatment for sickle cell disease late last year.

Executives surveyed anticipate similar to slightly higher levels of partnering in 2024, with buyers, Syneos reports, more bullish about striking traditional licensing arrangements—expecting sellers to continue to seek out partners given the still-likely constrained capital markets and financing picture. At the same time, the report notes that “sellers with the right molecule may spot attractive opportunities to partner with larger, integrated service providers offering flexible and scalable capability to help cope with evolving needs.”

The apparent tighter vice on pending deals of late by the FTC, and contentions of anticompetitive practices, have clouded the licensing picture somewhat as well. Notably, in December, Sanofi decided to terminate its proposed acquisition of an exclusive license to finance further development of Maze Therapeutics’ experimental drug for Pompe disease, which has completed Phase I trials.5 The partnership was first announced last May. The FTC decided to challenge the arrangement, claiming it would create a monopoly for drugs to treat the rare and potentially fatal genetic condition. Sanofi, in its statement,6 cited the delay and protracted litigation for pulling out of the deal, which the FTC had valued at $755 million.

“That set off some concerns and alarm bells,” says Abrams. “We have to better understand exactly what it was that the FTC found objectionable there. But, overall, deals like that will continue.”

There is similar sentiment around the M&A-FTC dynamic as well. The agency’s challenge last year of the Amgen-Horizon union and its antitrust review of Pfizer-Seagen (both deals were ultimately settled and cleared, respectively) triggered worries at the time of potentially dampening dealmaking appetites. Though acknowledging that the FTC will likely remain focused on biopharma (the agency contends industry consolidation has contributed to rising healthcare costs), S&P Global, in its report, doesn’t believe the continued scrutiny will put a dent into M&A volumes in 2024. Acquisitions, however, may take longer to complete in this heightened climate, S&P Global adds.

“It is a deterrent, but it’s not stopping companies from pursuing deals,” Baral tells ACT. “Maybe there will be higher thresholds that they’ll have to clear with the regulators to get the deal approved.”

IRA IMPLICATIONS

The potential ripple effects from the IRA on dealmaking aggression may be more complicated to track—particularly with the legislation’s uncertain fate in an election year. The bill, passed in August 2022, allows the Centers for Medicare & Medicaid Services (CMS) to negotiate prices on certain expensive and branded prescription medicines. CMS’s first 10 drugs to be negotiated were announced in August 2023, triggering several lawsuits from Big Pharma. A report issued this month by Vital Transformation argued that a proposed expansion to the IRA, which would increase government price setting to up to 50 selected Medicare drugs starting in 2029—and extend the program to the commercial market—would severely hamper the biopharma industry, including, the report says, $55 billion in lost partnership investments for the most impacted companies.7 The healthcare consultancy also alludes to “current drops in investments since the introduction of the IRA.”

Likely swaying such investment decisions today, Abrams says, is the IRA’s favorable position on new large-molecule biologics compared to small-molecule drugs. Provisions allow the former 13 years of immunity from mandated price negotiations, while setting a nine-year exemption period for the latter.

“It’s likely to tilt the M&A surge toward large-molecule drugs. What that could translate to is a very real strategic shift in pipelines toward biologics,” Abrams tells ACT. “The legislation has effectively raised the risk and shortened the timeframe where manufacturers can hope to recruit their investment in any new medicine.”

A BENEFIT FOR BIOTECH?

Such IRA drug distinctions could theoretically boost the impetus around efforts to revive the IPO market in biotech. After a quiet 2023, venture capital-infused activity in the life sciences has shown signs of life early in the new year,8 aligning with expert sentiment of an expected, gradual uptick and resetting of sorts for biotech valuations. This may bode well for the perhaps preferred deal targets of today: young startup and emerging clinical-stage companies with promising and differentiated therapies in development. For example, Syneos’s survey found that those companies focused on artificial intelligence (AI)-based discoveries—or attempting to advance biopharma-specific technology innovation—may attract buyers at premium prices for much of 2024.

Of course, despite the optimistic signs of late, and the synergy with Big Pharma’s dealmaking surge in benefitting the wider ecosystem, investment challenges remain, including the still “disconnect between where Big Pharma is interested in versus where biotech needs money,” says Baral. He points as well to the added hoops and assurances VCs are asking for today when deciding whether to fund early proof-of-concept assets to the maturity levels normally needed to attract interest and engagement from large pharma.

“Biotech has always been a very resilient industry; it’s in its DNA,” adds Baral. “… But [VCs] are very selective in where they are going to put their investment. The thresholds are much higher for a lot of these companies to prove why someone should invest in their technology and science.”

Baral, nevertheless, sees the door open for additional flurries of IPO activity and investment in the coming months. Private equity-backed financing is also poised to return to the scene more actively this year, experts believe, as well as other funding structures to help support R&D activities and advance hopeful new medical treatments and interventions.

“The FOMO (fear of missing out) factor it at work for some of the investment community, but there’s a high level of perceived risk as well,” says Abrams. “I think the issue is whether the investors that focus on that space get bolder and less risk-sensitive. … There are a lot of considerations in driving this business and obviously there are potential big payouts, too. But you really have to negotiate the business end of it. What it takes to do that is changing day by day.”

References

- 2024 EY M&A Firepower Report. EY. January 8, 2024. https://www.ey.com/en_gl/life-sciences/mergers-acquisitions-firepower-report

- Pharmaceutical and Life Sciences: US Deals 2024 Outlook. PwC. December 2023. https://www.pwc.com/us/en/industries/health-industries/library/pharma-life-sciences-deals-outlook.html

- Industry Credit Outlook 2024: Healthcare. S&P Global Ratings. January 9, 2024. https://www.spglobal.com/ratings/en/research/pdf-articles/240109-industry-credit-outlook-2024-healthcare-101591892

- 2024 Dealmakers’ Intentions Survey. Syneos Health. January 2024. https://go.syneoshealth.com/l/63102/2024-01-08/4s5w6q/63102/1704748007nciyoFDi/Syneos_Health_Dealmakers_Report_2024.pdf

- Sanofi Terminates Deal on Drug License After US FTC Objects. Reuters. December 11, 2023. https://www.reuters.com/business/healthcare-pharmaceuticals/sanofi-terminates-deal-drug-license-after-us-ftc-objects-2023-12-11/

- Press Release: Statement on FTC Challenge to Proposed License Agreement with Maze Therapeutics. Sanofi. December 11, 2023. https://www.sanofi.com/en/media-room/press-releases/2023/2023-12-11-21-08-20-2794272

- The Impact of the House Proposed IRA Expansion on the US Biopharma Ecosystem. Vital Transformation. January 18, 2024. https://vitaltransformation.com/wp-content/uploads/2024/01/House-Dem-IRA-Bill-VT-Research-FINAL-01172024.pdf

- Slabodkin, G. 2024 Brings Surprising Early Surge of Biotech IPOs. BioSpace. January 19, 2024. https://www.biospace.com/article/2024-brings-surprising-early-surge-of-biotech-ipos-/?s=89

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://www.appliedclinicaltrialsonline.com/view/the-twists-and-turns-in-biopharma-dealmaking-2024-trends